Credit Impact

Liberty Debt Relief and Your Credit Score

Our first priority in this program is to reduce and resolve your debt to strengthen your financial footing. While the end result is worth it, you’ll still face challenges, such as a credit score decrease during your first few months. But there’s good news—over the course of the program, your score should recover and even rise higher than it was before.

We conducted a four-year study that proves this claim, reveals exciting results for your financial health, and keeps you focused on the most important goal in the meantime: getting past your debt!

Credit score lowers—then rises back up

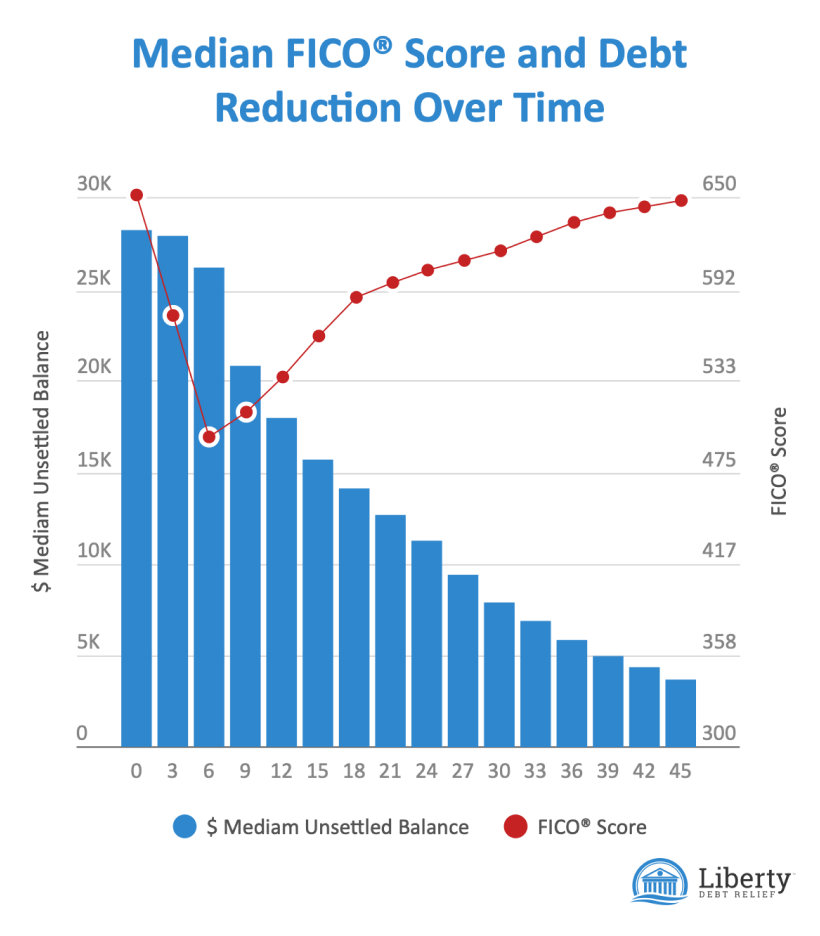

In our four-year study of Liberty Debt Relief clients, we tracked credit scores and unsettled debt over time. Here are the key points:

- Clients began Liberty Debt Relief with a median of $28,000 in debt and a 650 FICO® score.

- Within 6 months of enrolling, the median FICO® score dropped 150 points.

- After 45 months, clients had a median of $3,800 in debt and a 648 FICO® score.

Takeaway: Graduates enjoy a steady credit score uptick. This increase comes partly from a much lower debt burden. But it’s also due to the healthy financial habits that graduates learned in the program, put into practice to keep moving forward financially.

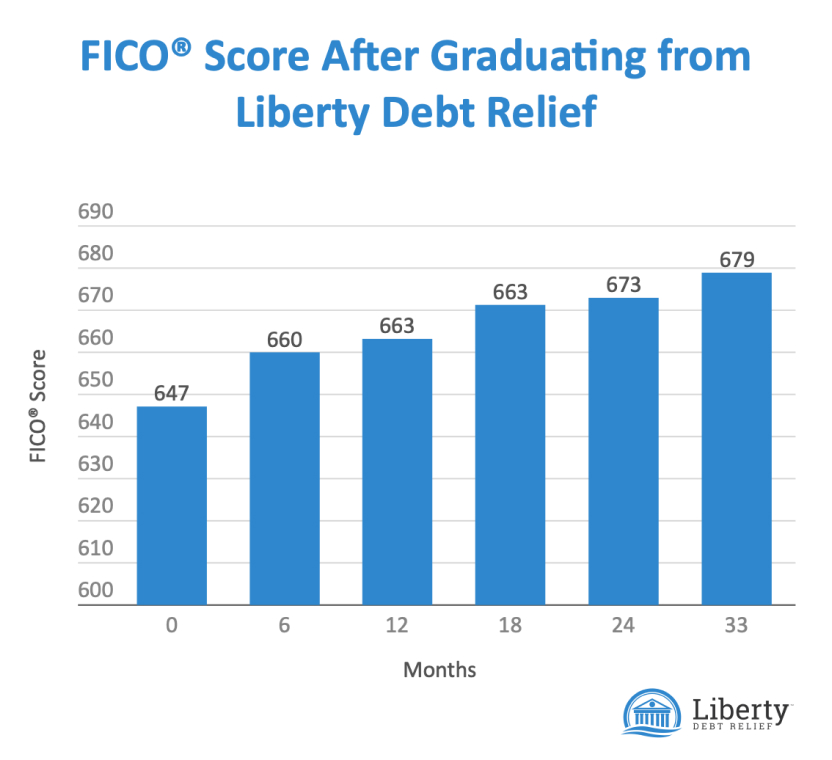

Increased score after Liberty Debt Relief

After your debts are resolved and you graduate from Liberty Debt Relief, your credit health should continue to strengthen. Here’s the study data to back up that claim:

- Graduates’ scores increased for the remainder of the study, ending far higher than at the start of Liberty Debt Relief.

- Within 18 months, grads reached a 671 median FICO® score.

- 670 is the threshold of a “good” FICO® score, which makes qualifying for competitive rates easier.

Takeaway: Graduates enjoy a steady credit score uptick. This increase comes partly from a much lower debt burden. But it’s also due to the healthy financial habits that graduates learned in the program, put into practice to keep moving forward financially.

Signaling hardship: why the decrease matters

Here’s why your credit score will decrease in the early stages of your program, and why that decrease actually plays to your advantage. (Yes, you read that right.)

- For the program to work, you have to decide to stop paying your creditors.

- Stopping payments causes your accounts to go delinquent, which demonstrates your financial hardship to creditors.

- Once creditors understand you have a hardship, that opens the door for Liberty Debt Relief to negotiate and reduce the amount you owe.

Stopping payments will lower your credit score. However, stopping payments is the only way that creditors will be willing to accept less on a debt. In other words, the action that can lower your credit score can also lower your debt.

Since we’ve shown that the credit score impact is temporary, your program is ultimately worth it for the end results: reducing what you owe, resolving your debt, and improving your overall financial standing—including a recovered credit score.

“They came through, scary at first because my credit score plummeted but after a year of making my set payments I was able settle with the majority of my accts slowly but surely my credit score is going back up.”

Remember, your financial health is more than just a number

It makes sense to be concerned about your credit score, considering how much it gets emphasized in ads. But it might be helpful to understand what a credit score represents (and what it doesn’t represent) to see that it makes up only one part of your financial health.

Consider this: Your credit score measures your risk level to creditors for lending. Since you’re in this program to get rid of debt, it doesn’t make sense to take on more debt right now. For that reason, it’s okay if your credit score isn’t the best while you’re busy putting your debt behind you.

Once you graduate from Liberty Debt Relief, your debt burden will be significantly lower and your credit score should be back to what it was before you enrolled—if not higher. At that point, you’ll have more options for financing AND you’ll be able to use the healthy financial habits you learned in the program to avoid getting back into debt.

Learn more about your credit score in Liberty Debt Relief—and how it puts you on a better path financially in the long run.